Economic Slowdown and Energy Prices Currently Burden European and German Production

In the short term, the economic development and the still high energy costs are burdening the German foundry industry. Production and order intake are likely to be significantly below the previous year's level on average in the industry this calendar year. The European industry association CAEF's sentiment survey recently provided signs of a slight successive improvement in the situation, which recorded an increase in the indicator for the third consecutive month in March 2024.

For more Facts an Figures (27 pages) please check the associated Whitepaper here

Medium- and Long-Term Industry Trends Provide Impulses

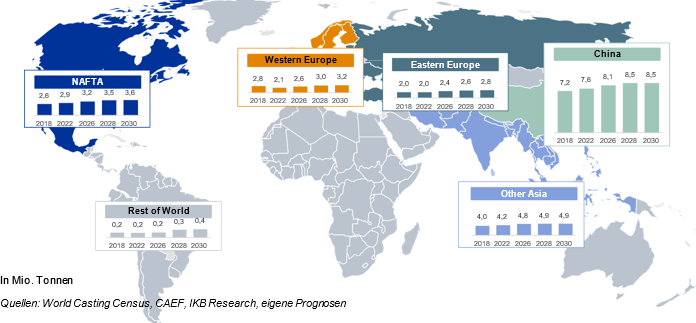

The opportunities and challenges of the foundry industry are heterogeneous, depending on the product spectrum and customer industries. After the recent recovery, automobile production will grow only slightly in Europe and North America in the medium and long term but will remain a relevant sales market for cast products. This is especially true for iron and steel casting in the medium term due to the slower-than-expected ramp-up of electromobility in Europe. Stronger impulses are expected from the commercial vehicle market due to upcoming fleet modernizations. A special economic boom is expected in North America in 2025 and 2026 for all commercial vehicle classes over 65 tons due to significantly stricter EPA emission standards starting from the 2027 model year. Overall, aluminum casting will continue to gain importance with the ramp-up of electromobility and the trend towards lightweight construction. The global mechanical engineering sector is expected to see a strong increase in sales by 2030. Important impulses are provided by ongoing digitization and the associated need to modernize the machinery. The global construction industry also remains on a long-term growth path, with infrastructure projects being the main driver. The planned expansion of wind energy in Europe will provide impulses for demand from the energy sector.

Casting Forecast Dependent on Data Situation and Geopolitical and Technological Assumptions

So far, IKB's forecasts for the global foundry industry have been based on the annually published data of the Modern Casting Census. However, the production data for 2022 have not been published by mid-April 2024, contrary to the historical cycle. For this reason, the figures underlying the forecast for 2022 are partly estimates or based on rudimentary press reports. Therefore, the current casting forecast is provisional and could be adjusted if a different overall picture emerges when a current Modern Casting Census is published concerning historical production data.

Geopolitical assumptions include that the Russia-Ukraine war will end within the next two years, that the current conflicts in the Middle East will not spread to other neighboring states or will be resolved in the Gaza Strip by mid-2025, and that no new conflicts with international ramifications will break out in Asia.

The impact of the technological developments mentioned in the section on industry trends in electromobility, mechanical engineering, and the energy sector on the forecasted production figures is based on current capacities and supply chains. Geopolitical developments, increased resilience efforts by the EU, and industrial policy programs like the IRA in the USA can therefore lead to regional shifts in the forecasted production figures.

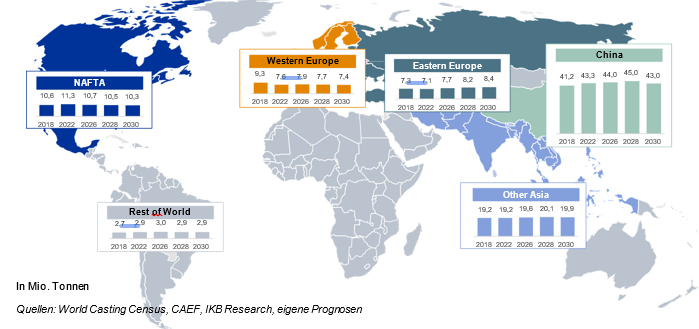

Global Iron and Ductile Iron Casting: Contrasting Developments

In 2020, the COVID-19 pandemic caused a sharp decline in iron casting production, and by 2022 only a few regions had returned to 2018 levels. China was able to expand its dominant position in the short term but will be burdened by lower demand from the construction sector in the long term. Japan and Korea will also lose market share. The rest of Asia will develop on average, like the rest of the world. India, which has a high demand for infrastructure investments, is experiencing stronger growth; Vietnam and Indonesia will follow in the coming years. Within Europe, stronger growth is expected in Eastern European countries, including Turkey, which is still burdened by Russia's war in Ukraine. Spain could benefit in the medium term from the wind energy boom.